Note

Go to the end to download the full example code. or to run this example in your browser via Binder

非负最小二乘法#

在这个示例中,我们拟合了一个对回归系数施加正约束的线性模型,并将估计的系数与经典线性回归进行比较。

import matplotlib.pyplot as plt

import numpy as np

from sklearn.metrics import r2_score

生成一些随机数据

np.random.seed(42)

n_samples, n_features = 200, 50

X = np.random.randn(n_samples, n_features)

true_coef = 3 * np.random.randn(n_features)

# 将阈值系数调整为非负值

true_coef[true_coef < 0] = 0

y = np.dot(X, true_coef)

# 添加一些噪音

y += 5 * np.random.normal(size=(n_samples,))

将数据分为训练集和测试集

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.5)

拟合非负最小二乘法。

from sklearn.linear_model import LinearRegression

reg_nnls = LinearRegression(positive=True)

y_pred_nnls = reg_nnls.fit(X_train, y_train).predict(X_test)

r2_score_nnls = r2_score(y_test, y_pred_nnls)

print("NNLS R2 score", r2_score_nnls)

NNLS R2 score 0.8225220806196525

Fit an OLS.

reg_ols = LinearRegression()

y_pred_ols = reg_ols.fit(X_train, y_train).predict(X_test)

r2_score_ols = r2_score(y_test, y_pred_ols)

print("OLS R2 score", r2_score_ols)

OLS R2 score 0.7436926291700346

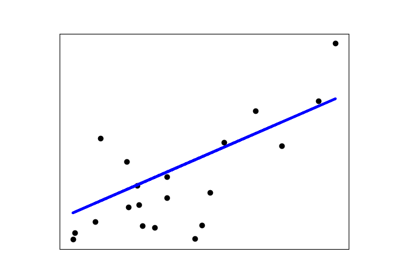

比较OLS和NNLS的回归系数,我们可以观察到它们高度相关(虚线是恒等关系),但非负约束将一些系数缩减为0。非负最小二乘法本质上会产生稀疏结果。

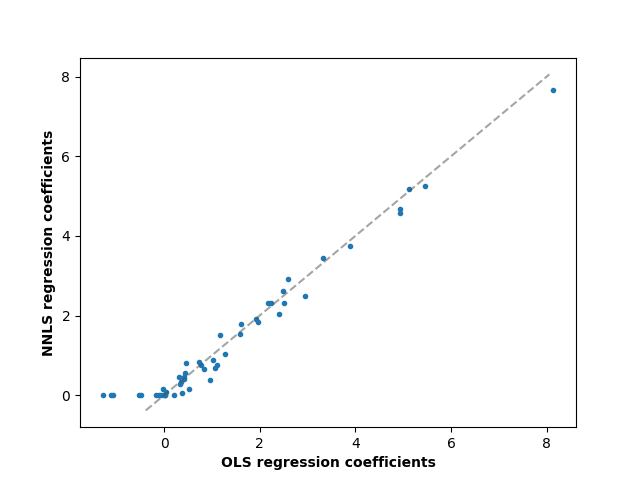

fig, ax = plt.subplots()

ax.plot(reg_ols.coef_, reg_nnls.coef_, linewidth=0, marker=".")

low_x, high_x = ax.get_xlim()

low_y, high_y = ax.get_ylim()

low = max(low_x, low_y)

high = min(high_x, high_y)

ax.plot([low, high], [low, high], ls="--", c=".3", alpha=0.5)

ax.set_xlabel("OLS regression coefficients", fontweight="bold")

ax.set_ylabel("NNLS regression coefficients", fontweight="bold")

Text(55.847222222222214, 0.5, 'NNLS regression coefficients')

Total running time of the script: (0 minutes 0.031 seconds)

Related examples